I once again present you with the very interesting findings of the research done by EMCS – http://www.emcs.com.mt ; which was carried out between Tuesday 12th May and Friday 15th May 2020. In total 498 individuals aged 18 and over were interviewed, with data being representative of the local population in terms of gender, age (18 and over) and location of residence, with a margin of error of +/- 3.4% at 95% confidence interval.

The findings are most interesting as there are certain shifts from the perceptions of the Maltese a few weeks ago. The main findings are:-

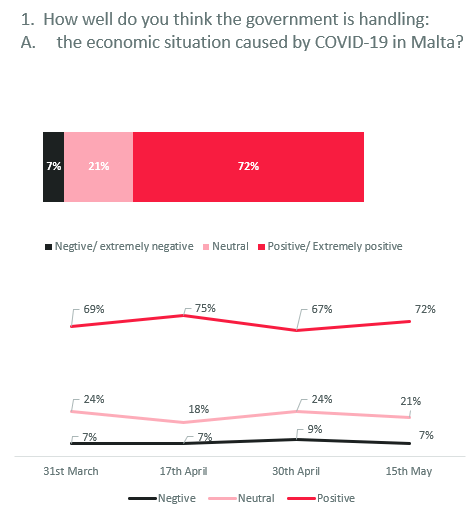

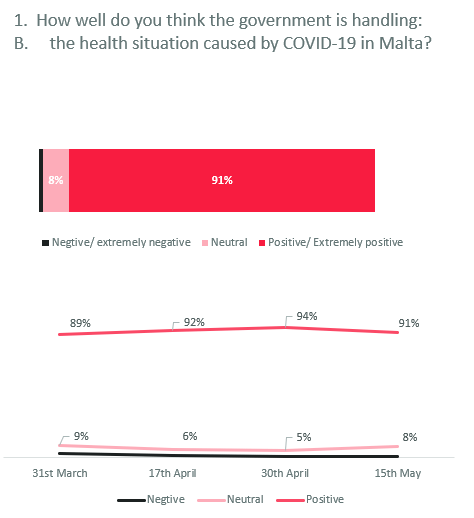

In line with past surveys, the Maltese are overall satisfied with the way the government is handling the COVID-19 situation, both in terms of the health situation and the economic one. 72% of the general public is of the opinion that the government is handling the economic situation caused by COVID-19 in Malta well. Locals’ positive perception increased marginally (by 5%) when compared with the study conducted 2 weeks ago, though overall locals still have stronger positive views to how Government is handling the health situation (91% positive views as opposed to 94% 2 weeks ago).

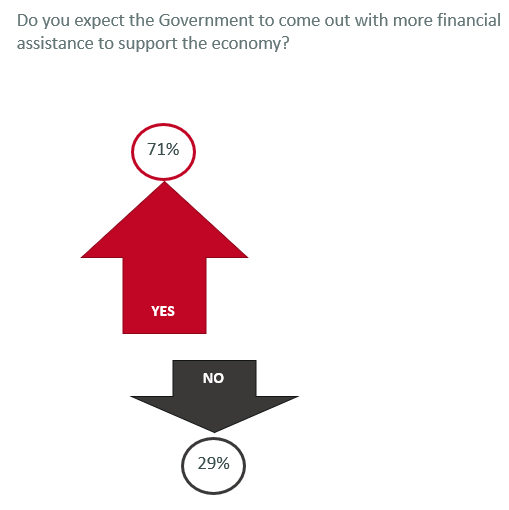

71% expect the Government to come out with more financial assistance to support the economy (78% in the previous study).

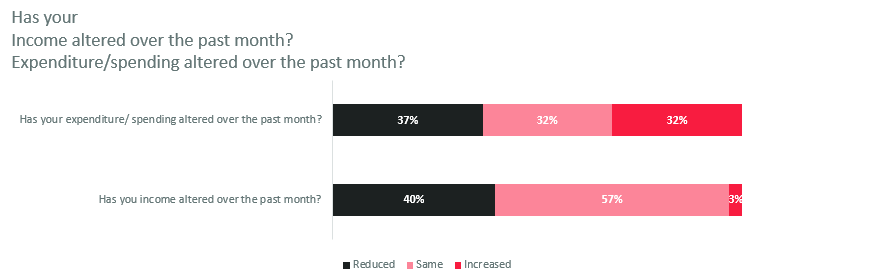

57% of respondents indicated that their income had remained stable over the past month. Conversely, 40% indicated that their income had decreased. (Of these, 19% indicated that it had slightly decreased while 21% indicated that it had reduced considerably). This represents a marginal increase since 2 weeks ago (then 33% had indicated a decrease). 53% of those aged 25 to 44 indicated that their income had decreased this being the highest cluster.

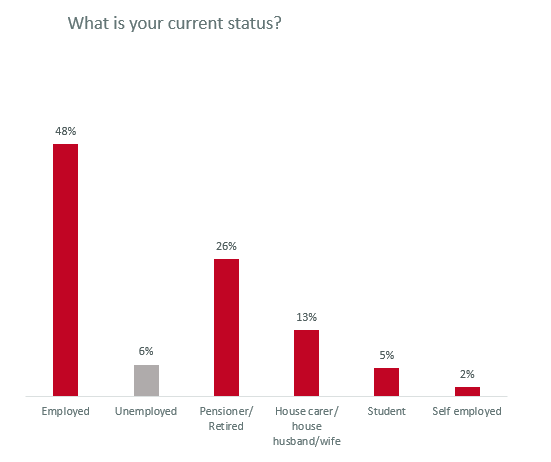

A total of 6% of the population indicated being unemployed. This is in line with the study conducted 2 weeks ago.

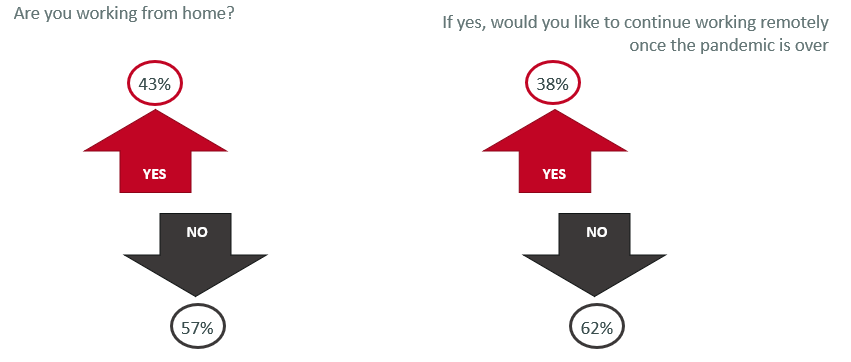

Among those in employment, 43% indicated to be working from home. This represents a decrease of 12% since the previous study. Furthermore, the majority of those working from home indicated a preference to return to the workplace once the pandemic is over (with only 38% indicating a willing ness to continue to work remotely).

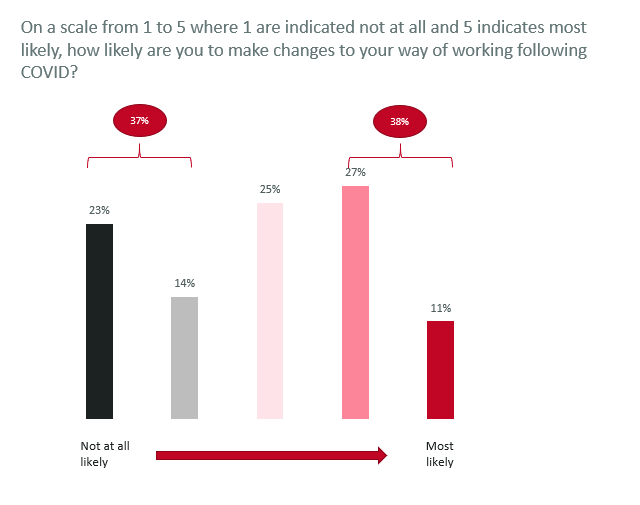

38% are inclined to make changes to their way of working following COVID-19.

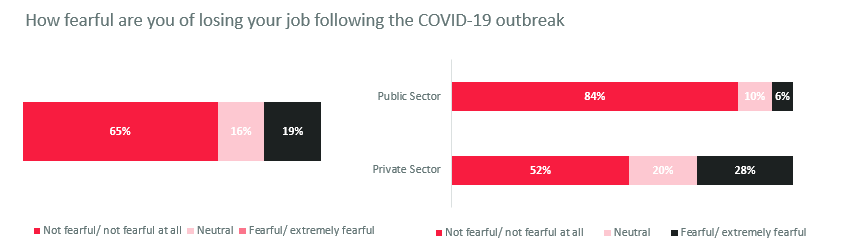

With 65% responses, overall individuals who are currently in employment do not fear losing their job. That said, 19% are fearful (12% fearful and 7% extremely fearful). This represents an increase of 8% over the previous survey.There are variances in responses between those working in the private sector as opposed to those in the public sector. 84% of those in the public sector are not fearful/ not fearful at all as opposed to 52% of those in the private sector. While the figure of those in the public sector has remained consistent (83% in the previous study), 28% of the private sector are fearful, an increase of 13% over the previous study.

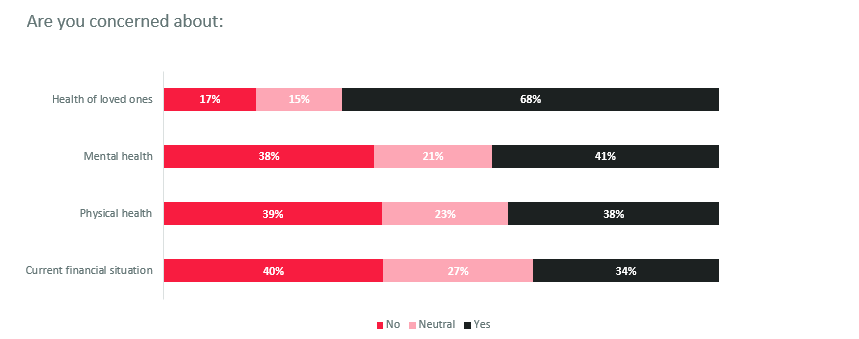

A review of locals’ concerns on a number of factors evidences that overall locals’ main concern relates to the health of their loved ones and those close to them (68%). Such figure are in line with the study conducted 2 weeks ago.

34% of respondents indicated being concerned of their financial situation (18% slightly, 16% a lot). This is in line with the previous study (then 36%).

In terms of expenditure, 32% indicated that their expenditure had not altered over the past month. 37% indicated that their expenditure had decreased while 32% indicated that it had increased. Such figures are consistent with the study conducted 2 weeks ago. A review of responses by age indicates that those indicating an increase in expenditure increased with age, with the highest percentage being registered among those aged 65 and over (45% of those within this age bracket).

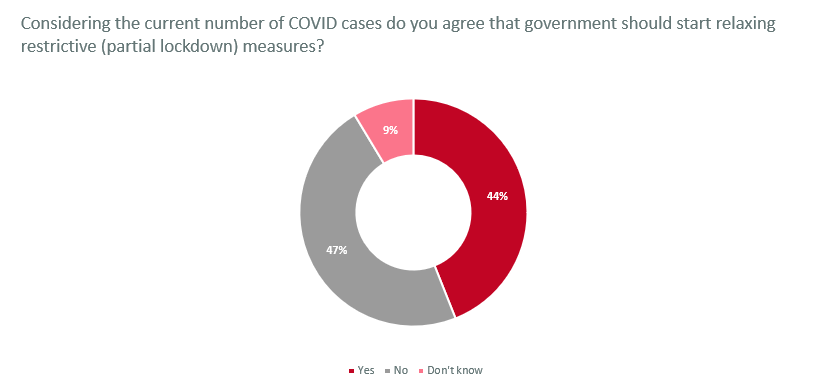

44% of respondents agree that the government should start relaxing restrictive (partial lockdown) measures. This represents a considerable increase over the previous study. 2 weeks ago 26% were in agreement. 47% do not agree (2 weeks ago the percentage of those that disagreed stood at 66%).

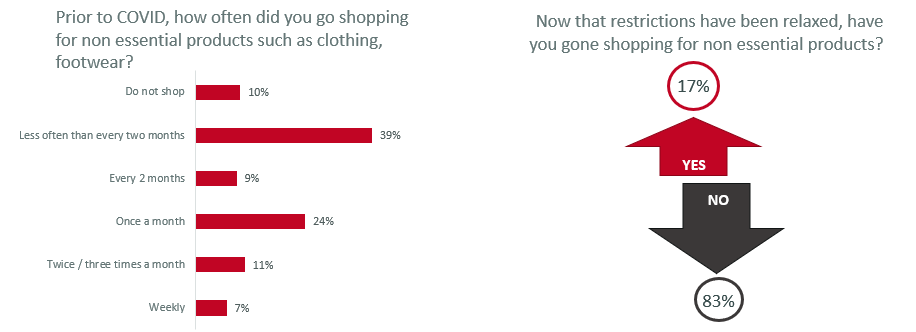

A review of respondents’ attitudes towards shopping for non essential items (such as clothing, footwear etc) evidences that COVID-19 is not likely to impact considerably consumers’ purchasing trends among regular shoppers (those that shop every 2 months or more often). Prior to the COVID outbreak 51% of respondents indicated shopping for non essential products once a month or more often with 18% indicating to do so twice to three times a month or more often. Following the relaxation of restrictions, 17% of locals had gone shopping. Among those that had not yet gone, 10% indicated their likelihood of going within one month, while another 21% indicated their likelihood to go shopping for non essential products within 2 months.

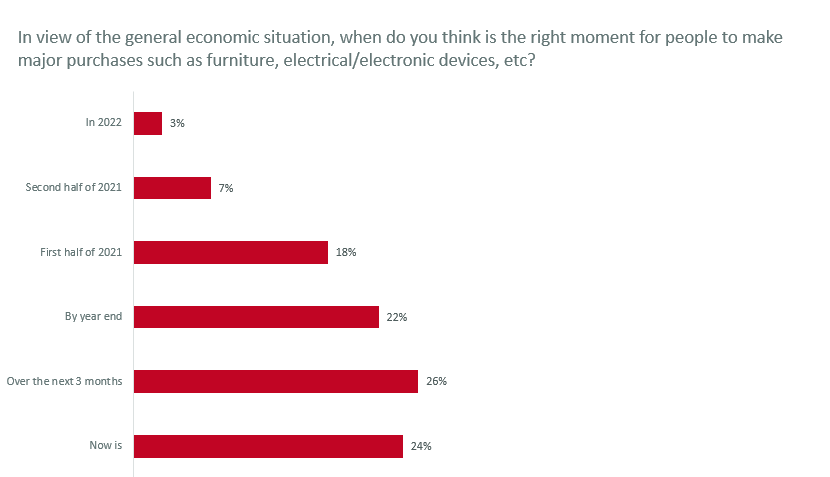

Mixed views were noted when analysing consumers’ opinions with respect to major purchases such as furniture, electrical/electronic devices. 24% of the population think that now is the right moment for people to make major purchases such as furniture, electrical/electronic devices and similar, with another 26% indicating ‘over the next 3 months’ and 22% by year end. Conversely, 28% had conservative views with 25% indicating that it would be opportune to wait until 2021, with 3% indicating to wait till 2022.

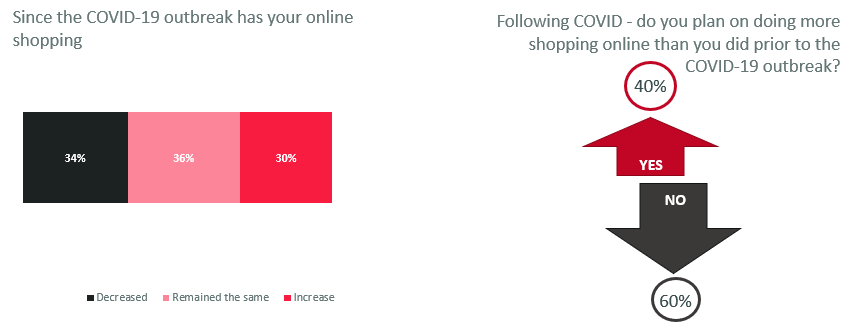

Likewise, mixed views were observed with respect to online shopping trends following the COVID-19 outbreak. 30% indicated that their online shopping hand increased while 34% indicated a decrease. Once COVID is over 40% plan on doing more shopping online than they did prior to the COVID-19 outbreak.

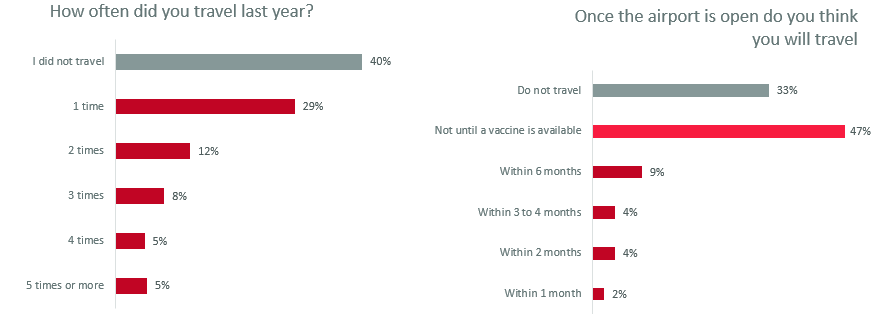

Travelling is likely to be considerably impacted by COVID-19. A review of travel habits evidences that last year 60% of respondents had travelled at least once. Nonetheless, 19% indicated their likelihood of travelling within 6 months or more often once the airport is open. Conversely, 47% will wait until a vaccine is available prior to travelling.

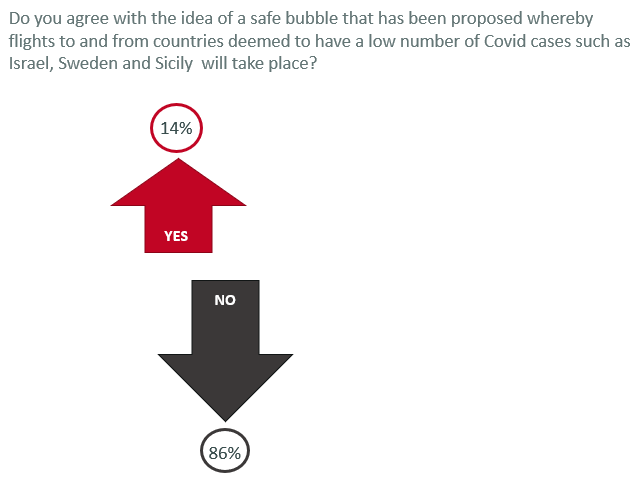

Furthermore, the vast majority of respondents (86%) do not agree with the idea of a safe bubble that has been proposed whereby flights to and from countries deemed to have a low number of Covid cases such as Israel, Sweden and Sicily will take place.

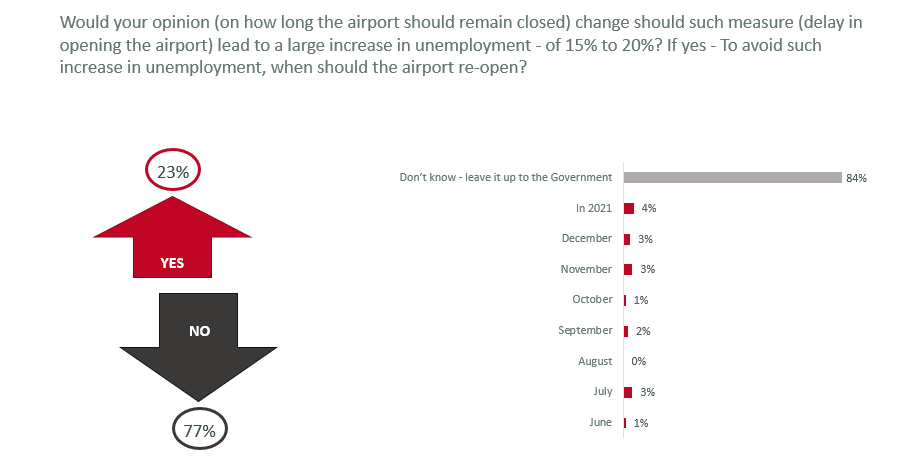

The general public does not think that the Government should open up the airport any time soon, with only 10% indicating that this should be done some time this year. Furthermore, the majority of the population (77%) are not ready to change their opinion, even if such a decision would result in an increase in unemployment (of between 15% and 20%). Such figures are consistent with results collated 2 weeks ago.

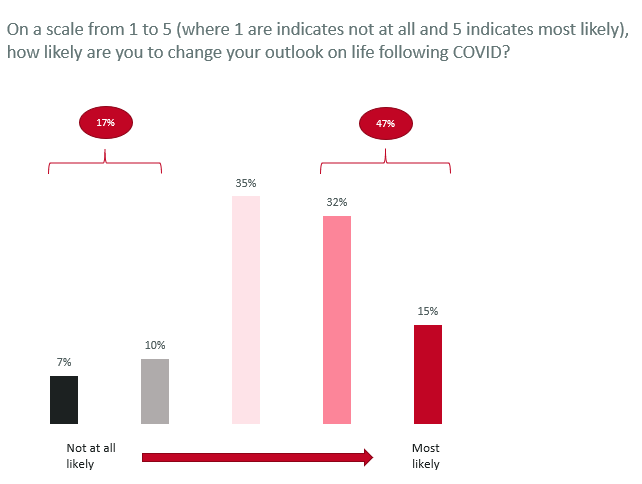

47% of respondents are likely to change their outlook on life following COVID (of these 32% indicated that it was likely while 15% indicated that it was most likely). Although marginally higher, this figure is consistent with the previous study (then 43%)

Conversely, 17% indicated that it was unlikely that their outlook on life to change.

The findings in more detail can be seen here below:-

•Locals’ positive perception increased marginally (by 5%) when compared with the study conducted 2 weeks ago.

•The survey evidences a marginal decline in peoples’ positive perception as to how the health situation is being handled.

•In line with the previous study, there was no variance when analysing responses by those that work in the private and public sector.

•A total of 6% indicated to be currently unemployed. Such figure being consistent with previous studies.

•Of the unemployed (30 individuals) 43% indicated to have been in employment a month ago. 85% within this cluster (11 individuals) indicated to have been made redundant following the COVID-19 outbreak.

•This figure represents a decline over the previous study. Then 55% had indicated to be working from home.

•Furthermore, the majority of those working from home (62%) would prefer to work from their place of work rather than remotely once the pandemic is over.

•Conversely, 38% indicated that it was likely/ most likely that they would make changes (35% in the previous study).

•That said, 19% are fearful (12% fearful and 7% extremely fearful). This represents an increase of 8% over the previous survey.

•There are variances in responses between those working in the private sector as opposed to those in the public sector. 84% of those in the public sector are not fearful/ not fearful at all as opposed to 52% of those in the private sector.

•28% of the private sector are fearful, an increase of 13% over the previous study.

•Those in the public sector that are fearful has remained consistent (5% 2 weeks ago).

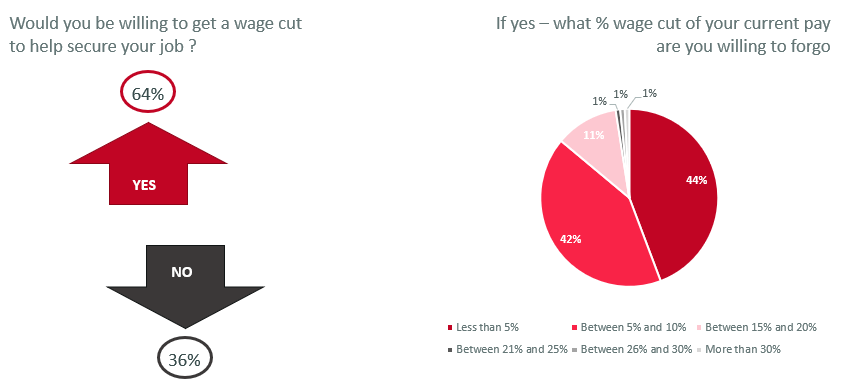

•Those willing to get a wage cut increased marginally (previously 57%). Within this segment 86% would be willing to forgo 10% of their wages or less.

•In terms of expenditure, 32% indicated that their expenditure had not altered over the past month. 37% indicated that their expenditure had decreased while 32% indicated that it had increased. Such figures are consistent with the study conducted 2 weeks ago.

•A review of responses by age indicates that those indicting an increase in expenditure increased with age, with the highest percentage being registered among those aged 65 and over (45% of those within this age bracket).

•Following the relaxation of restrictions, 17% of locals had gone shopping.

•Among those that has not yet gone, 10% indicated their likelihood of going within one month, while another 21% indicated their likelihood to go shopping for non essential products within 2 months.

•Such figures imply that among regular shoppers (those that shop every 2 months or more often), COVID-19 is not anticipated to alter considerably their shopping habits.

•Conversely, 28% had conservative views with 25% indicating that it would be opportune to wait until 2021, with 3% indicating to wait till 2022.

•While 30% indicated that their online shopping had increased, 34% indicated a decrease.

•40% plan on doing more shopping online than they did prior to the COVID-19 outbreak.

•Nonetheless, 19% indicated their likelihood of travelling within 6 months or more often once the airport is open.

•Conversely, 47% will wait until a vaccine is available prior to travelling.

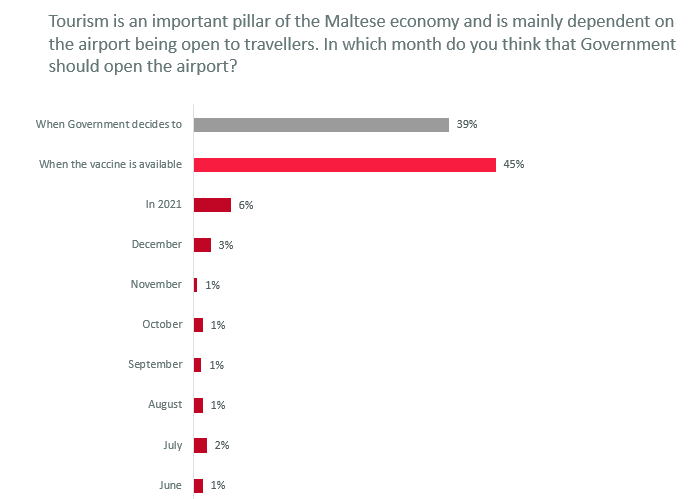

•39% trust in the Government to decide when its best.

•45% are of the opinion that the airport should only open up once a vaccine is available.

•Even among those that answered in the positive (23%), those that believe the airport should re-open any time soon are minimal (13%).

•Conversely, 17% indicated that it was unlikely that their outlook on life to change. (2 weeks ago this stood at 22%)

•Overall, locals concerns altered marginally.

•41% are concerned about their mental health, with 34% concerned about their financial situation.